America’s Financialization and Economic Decay

“…According to the rigor of the law, the emperor might have asserted his claim, and the prudent Atticus prevented, by a frank confession, the officiousness of informers. But the equitable Nerva, who then filled the throne, refused to accept any part of it, and commanded him to use, without scruple, the present of fortune. The cautious Athenian still insisted, that the treasure was too considerable for a subject, and that he knew not how to use it. Abuse it then, replied the monarch, with a good- natured peevishness; for it is your own.”

– Edward Gibbon, Decline and Fall of the Roman Empire

Has America bestowed a similar license upon its modern-day patricians?

Our American economy, once the preeminent industrial power of the globe, now stumbles in the darkness cast by China’s long shadow. The forlorn state of America’s industrial sector stands dwarfed by the gluttonous and bloated financial sector–the primary source of revenue and “growth” today. How could it be that America, at one point accounting for half of the world’s manufacturing, has so prodigally mortgaged its productive power? The answer lies within the capricious deregulation of banks, the ascendancy of the shareholder-primacy paradigm, and the offshoring of our industries.

Can America retain its economic majesty when it produces so little yet consumes so very much? Can America stand the test of time when its economy is one of paper and ink, while our competitors like China maintain an industrial labor force of a hundred million? Shall the arsenal of democracy prevail without its arsenal? Will America remain the land of opportunity, or succumb to shareholder opportunism? The time has come for Americans to address these questions. The catechesis of economic theorists has proved to be fallible, and the time has come to nail our theses to the cathedral doors of the Chicago School, heretics though we may be.

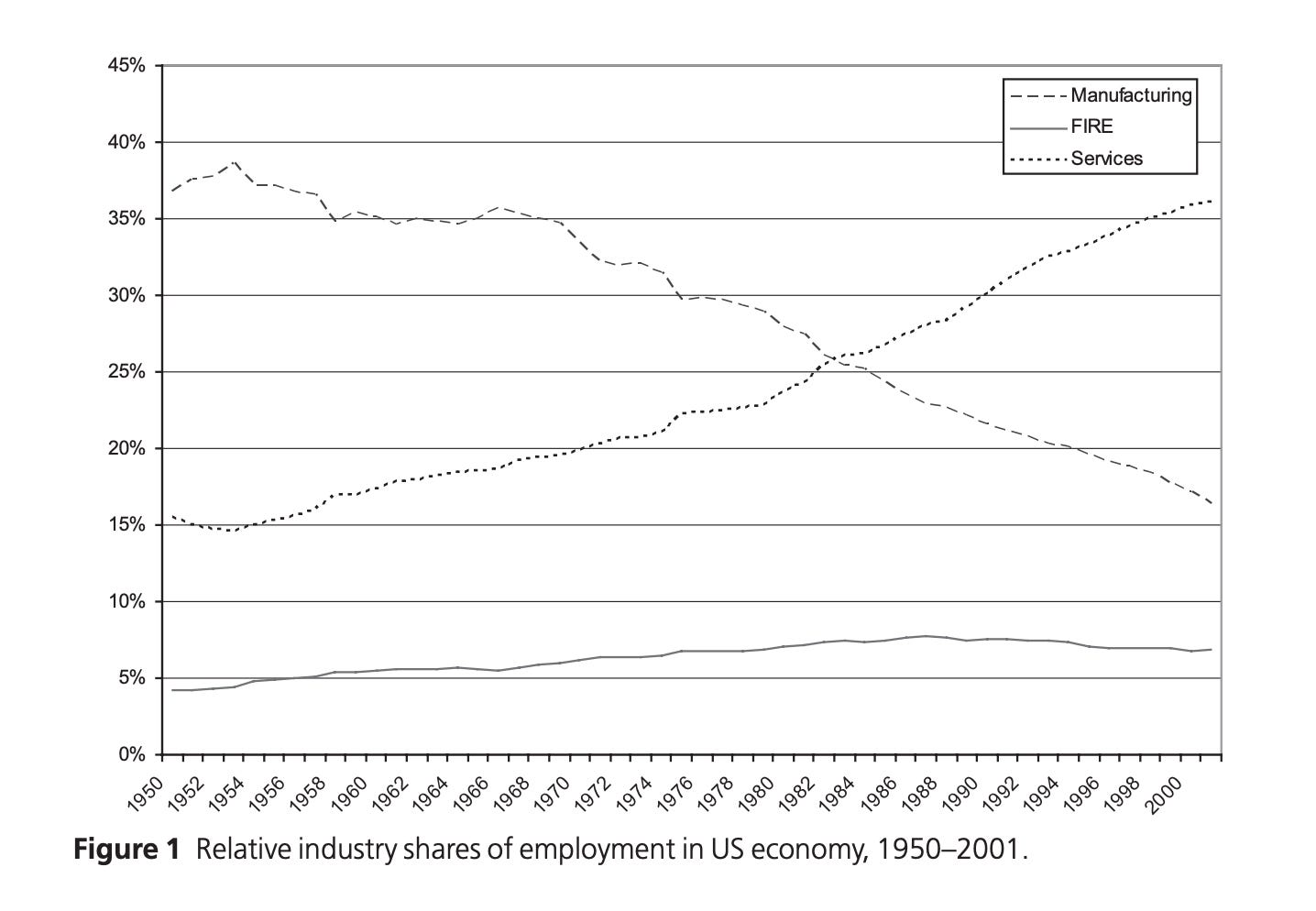

Like Esau, we have sold our birthright for a bowl of lentils. The finance sector has surpassed the productive base that enabled American excellence in the economy, technology, and culture. By the early 2000s, 40% of corporate profits were attributable to finance1, all while manufacturing lost one third of its jobs during the first decade of the 21st century2. The contribution of the finance, insurance and real estate sector to GDP has doubled since 1945, whereas the contribution of manufacturing has evanesced, having dwindled by more than half3. This is the nature of financialization: the detumescence of productive assets and enterprises and the simultaneous rise of financial services and enterprises as the cornerstone of the economy.

This begs the question: why is financialization untenable? A financialized economy, an economy where the financial sector is the largest source of investment and the most profitable one, produces an ecosystem where investment capital prefers asset-light firms over firms with more costly assets, or firms whose assets and operations are not capital-intensive in that they require minimal reinvestment and not heavy amounts of physical labor. In other words, investors look for firms with less liabilities to put their money. Such a precept necessarily rules out manufacturing, as manufacturing requires intensive labor, time, and money to start up and maintain, a circumstance which shareholders addicted to immediate increases in share price and dividends do not wish to tolerate. The environment described drives executives to disaggregate capital-intensive assets from non-intensive ones as intellectual property, design, and/or services. Yet desultory investments hoping for a momentary increase in price–attempts to appease shareholders reminiscent of Ulysses’s ravenous plunderers–cannot replace a productive base for tangible, permanent goods with permanent demand. Our economy has been deprived of fundamental necessities and is now reliant on speculation and intangibles.

What has driven this shift toward shareholder preference for asset-light companies? In the age of financialization, the primary modality of corporate governance is shareholder primacy. Companies that have affirmed their credenda as the pursuit of delivering profits to their shareholders–a dogma heretofore scarcely scrutinized–have, in the same stroke, occasioned and given way to a raucous shareholder class which believes it is its right to have the capital of the company be put toward the maximal return of their investment–and sooner rather than later. This, however, has also made manifest what can be understood as a kind of accounting supremacy, or balance sheet supremacy. The executive, hoping to retain the investor capital needed to maintain the company and have any prospect of growth, must forgo any kind of expense or long-term cost which will appear on the accounting sheet in reports and lead investors to believe the company is beleaguered with expenses that defray profits. Necessary corporate reinvestment which conduces long-term growth of real assets and profit is thus discouraged. This has produced the startling statistic that half of current market capitalization resides in companies that, owing to their large shareholder dividends, are squeezed of profits and thus are unable to afford necessary corporate reinvestment. The desire for lean balance sheets and the appetites of the shareholder have necessarily directed a large amount of investor capital to the finance sector, a sector where speculation, securities, and services are the primary source of income, not capital-intensive assets. Non-financial companies must ship off their expensive assets to China, or lose investment. It is by the same token we have lost our manufacturing capacity and instead look to our financial sector for revenue. The means to reinvest in a company and enlarge its productive profile have been uprooted by the exclusionary pursuit of shareholder value. However, this conception of corporate governance, though widely disseminated, is not only unworkable but detached from American corporate law, as Lynn A. Stout explains in “The Myth of Shareholder Value.”4 To put it concisely, Stout asserts that the executives of a public corporation are afforded full discretion over the direction of company funds as long as it is done in good conscience and for the sake of the company’s growth. This concept is called the business judgment rule. Shareholders, Stout explains, simply own a contract which details their rights and when they are entitled to receive part of the company’s profits, which is in itself decided by executives. They are not owners, nor are they the sole claimant on the company’s residual profits (remaining profits after capital expenses). It is therefore necessary to reconsider the perception of shareholders and their relation to the public corporation (a corporation which publicly sells shares of stock), as executives respond to the interests of shareholders before those of the company sacrifices the long-term for the short-term–a tendency which has encouraged reducing liabilities and in so doing, our productive base. While shareholder primacy’s adamantine adulators assiduously asseverate that corporate action needs only augment the affluence of shareholders, this apparent auspice is most acerbic, as it were. Executives must wield the authority vested in them to make long-term decisions. This principle hearkens back to Adam Smith, who named frugality and thrift as origins of wealth; and indeed, America’s strength was always its ability to harness the energy of its people into nation-building enterprises. America’s visionary ability is now eclipsed by less-than-ecumenical stockholders.

Now, the attention of this article will be redirected to those elements which set in motion this preference for a financial economy, where the main stakeholders are shareholders, and not an industrial economy which also accounts for the long-term growth and welfare of communities, employees, and business owners alike. Financialization was precipitated largely by two factors: the deregulation of the banks and the acceptance of the shareholder-primacy blueprint, as described earlier. The origins of these two shall now be explained.

Before the 1980s, the financial sector was regulated to protect consumers and the economy at large from the concentration of speculative investment and financial power–a policy which was a reaction to a concentration of the same manner that took place prior to the Great Depression and contributed to it. What is the “concentration of speculative investment and financial power?” Concentration refers to power being vested in few financial entities, such as banks, the caprice of which has proven to be a destructive force. During this era of financial regulation, banking activity could not be carried out beyond state lines. Various activities such as deposit-taking, insurance, and investment banking required different entities–that is to say, different corporate bodies. However, the lack of growth and the high-inflation of the 1970s economy united the corporate sector in advancing and advocating deregulation. Delegating the reinvigoration of the economy to the free market, the hallmark of American prosperity, was a convenient exit strategy for a wearisome federal government. Thus, deregulation was the torrent from which emerged a multi-headed hydra; banks suddenly had access to several new aspects of the economy; interstate banking, expanded lending powers, investment and commercial banking were thus concentrated in the banks. The diminution of regulation, seen as a hindrance on the economy, fostered an environment in which what was apparently good for banks and business was thus good for the economy at large. The perfervid banks now sought to operate in all financial markets, and the extent of their imperial domain is reflected in the ostentatious fact that the top three banks in the U.S. now own over 35% of the assets in the banking sector, while more than half of the banking assets are controlled by only ten firms. A keen observer may ponder if the United States has not consigned its wealth and health to the avarice of its own extractive and gourmandizing patricians, the malediction of Rome.

But this Copernican revolution would be incomplete without its revolutionaries. Who is responsible for promulgating this new heliocentric (or rather, shareholder-centric) model? Who was its Copernicus? Enter Milton Friedman.

Deregulation and shareholder primacy were inculcated into the intellectual centers of society and corporate thought by the advent of the Chicago School of Economics and the popularization of Austrian School principles. In a time of economic woes, they ushered in an opiate for the masses, as it were, in the form of a simple and formulaic method to repair the economy. A business needs only to tend to its shareholders. All other desirable aspects of a good economy, such as favorable wages, growth, and efficienc,y would follow suit. The great personality of Milton Friedman was the standard-bearer for this doctrine, whose pithy and accessible rhetoric made such a view all the more appealing. Milton Friedman’s ideas courted the approval of the public, gaining currency with his winning of the Nobel Prize in 1976 and his PBS show in the 1980s. But as America was soon to find out, deregulation is not a free lunch. Somebody has to pay for it.

As deregulation increased the competition of the financial sector (one of the principal goals of deregulation–reinvigorating the economy through competition which finance had a part in), naturally economic instability would increase. As financial institutions have an increasing number of prospects for growth, and as banks are free to pursue these options, competition and enterprising will naturally occasion the risking of assets owned by these organizations during the passion of their competition. Banks and financial firms took on more debt, and they partook in riskier investments. As a result, the highest amount of bank and thrift failures since the Great Depression was recorded in the 1980s5. Seeking to prevent bank runs (an exodus of deposit withdrawals in a time of uncertain futures for banks) and credit-flow disruptions (significant reduction in the availability of capital and credit, stunting economic growth), the federal government undertook deposit insurance6, whereby the government guarantees to replace a certain amount of money deposited by bank customers if lost, ensuring banks stay afloat and capital remains available, otherwise financial competition may lead to credit crunches and economic downturns. Such a policy was enacted with The Depository Institutions Deregulation and Monetary Control Act of 1980, a law that increased the deposit insurance limit from $40,000 to $100,000. However, this imprudent policy of deposit insurance encouraged banks to take on even more risk, as a significantly greater amount of their funds would be backed by the government. Deregulation thus increased government subsidization of bank recklessness. Indeed, the Savings & Loan crisis7, largely spurred by deregulation (deregulation relaxed lending restrictions, leading to more loans being issued as banks simultaneously took on more risk8), cost the United States government $160.1 billion9, of which approximately $132.1 billion was paid for by the taxpayer10. Indeed, deregulation was not a free lunch, and it was paid for by the taxpayer and economic stability. The policy of achieving economic stability with deposit insurance only was able to last in the short term as the caprice of banks would catch up to them rather acutely. With deregulation, the volume of bank loans increased exponentially. Banks began to accumulate gargantuan portfolios of securities, thus chaining their performance and well-being to that of many other firms. As such, it became much too great a risk to let banks to fail–an event which has now become the equivalent of a spark that ultimately razes a forest. And thus, the “too big to fail” doctrine was born. This is a crucial aspect of financialization, as powerful and extravagant banks have increasingly sought to make profits from derivatives, securities, and have created a viable opportunity for investment as traditional manufacturing and industries are offshored. Our real and productive economy has thus been vitiated by the insatiable appetite of the banks. The goose that lays the golden eggs has been killed, as it were.

Another tenet of financialization is the phenomenon of securitization–the conversion of financial assets into tradeable securities. Securitization has been made manifest chiefly by the desire of investors, portfolio managers, and firms to find new profits in the absence of industries and the production of tangible deliverables. What, then, is the subject of trading and investment (the term, at this point in time, being liberally applied)? Mortgages, credit card debt, student loans, business receivables, and other such derivatives–a contract which derives its value from another asset or agreement, rather than containing something of value directly–now are the main focus of investors. Banks now group together a set of loans, bring it to market as a security able to be traded, for instance. An investor who buys such a deal is not buying anything of value nor anything that produces value, but is rather betting on the debtor paying off their debts. This process of banks selling their loan contracts to debtors as securities is called debt alienation (a component of securitization), whereby the new owner of the debt is entitled to the payment. A demonstration of the folly of securitization in this manner is none other than the 2008 housing market crash, where the prospect of banks profiting from selling loans and mortgages as securities led to an increase in loan volumes, even to those who had poor credit, ultimately leading to a popping of this bubble where a vast amount of firms, pension funds, and institutional investors had an enormous amount of capital. As companies have pursued asset-lighting and more “efficient” operations, the financial sector was required to fill this gap. The demand for new returns, new investments, and the apogee of the financial sector, created a higher demand for financial market activity and for investments in finance. The replication of this pernicious cycle perpetuates a financialized economy. Money flows into speculation, prices of existing assets are driven up, and the government insures large financial institutions against the potential fallout. The private equity and hedge fund industries have generated hundreds of billions of dollars in revenue despite underperforming simple market indices. The rapine of private equity loads debt onto companies, squeezes them of their value, then sells them off, endangering livelihoods and communities. There is no regard for the dignity of the individual in such a process. Moreover, there is also no prospect for long-term economic growth.

With the advent of financialization, the majority of firms consume their fixed capital faster than they make new capital expenditures; companies are consuming, but they are not producing. According to American Compass, 49% of market capitalization was accounted for by eroders (a firm that consumes its fixed capital faster than it would make new capital expenditures, though they still pay shareholder dividends even though their EBITDA is sufficient enough to reinvest in their assets as well11. Whereas in the 1971-85 period, 82% of market capitalization resided in firms that made capital expenditures greater than its consumption of fixed capital (Sustainers), by 2017 this number fell to 40%. What does this tell us? Businesses are not reinvesting in their own assets, indeed their own long-term growth. They instead focus on two things which have been discussed in this article: 1. Delivering “value” to shareholders and 2. Investing in the financial sector. Eroders are replacing growers. Capital is spent, “value” is created, assets are dried up, shareholders are paid, and that is the standard for a successful enterprise in a financialized economy.

Our Chinese competitors are diligent, harnessing their industrial and economic power according to long-term national goals (Made in China, Belt and Road Initiative) that increase their military, industrial, and technological prowess. Our somnolent economic policy, on the other hand, prefers to rest in a complacent languor, not scrutinizing the commonplaces of free trade and financialization. No potent interest advancing these reforms has presented that possesses the impetus and willpower to resist the lobbying of large financial institutions. Even if there were to be more recognition of the facts, there is simply a lack of a strong voice on either the left or right wing that has defined a cogent industrial and economic policy that provides solutions; policymakers often prefer simple maxims and guidelines, likely a significant reason for their yielding to Chicago School ideas. The time has come for a new and bold economic policy that resolves the ills of deindustrialization, financialization, and shareholder primacy, while not uprooting the foundations of American prosperity through government excess. What must be done? The foundations are the following:

- Mobilize the vast amount of capital in the financial sector looking for investments.

The creative energies of capitalism must not be stifled in a mistaken attempt to reform. There is great potential in the entrepreneur’s pursuit of profit–this needs only to be calibrated for the sake of the national interest, not forced away under a collectivization scheme which would seek to extricate the profit motive. How can this be done? Make enterprises that invest in the American economy and its productivity profitable and attractive to investors. Subsidization of domestically based companies and manufacturing companies is largely insufficient, as it does not remove the hurdle rate that prevents investors from investing in the first place. Because such operations are long-term and expensive at first, investors in today’s economy would indeed prefer to seek a faster and more surefire return. Then, if subsidization alone does not make certain enterprises more profitable, what can? Incentivizing investment from the source will redirect capital and increase the capital access of domestic-based and productive companies. American Compass expanded upon the idea of an “American Innovation Fund,”12 where the government creates a fund where federal capital insures the dollars of private investment, absorbing potential blows, yet also claiming less of the return. Such a model is worthy of serious research and consideration, and is likely to be decisive in making the first leap necessary in reestablishing our industrial base. One benefit of financialization is that it has created a vast financial sector with tons of capital looking for new prospects for profit. Government efforts to make select industries profitable, then, will release the floodgates for an unprecedented amount of funds to flow back into industry.

- Prevent the destruction of productive enterprises by the private-equity market.

The private-equity market in the United States is worth trillions, and yet its main operation is making quick money at the expense of employees and communities. Leveraged buy-outs (LBOs) allow private equity investors to buy out a company by taking on debt and using the assets of the company that they did not spend time and money on as collateral, thus reducing their risk and providing an easy exit strategy. Their main strategy is often to liquidate and sell all assets, or remove liabilities and pawn off the company they obtained for cheap. Such a phenomenon contributes to the ongoing hollowing out of our industrial base, as massive private equity operations offshore and liquidate capital-intensive projects to have a more appealing offer when they sell the company. The nature of this operation is not one rooted in long-term growth, but an arbitrary scheme that often leaves workers unemployed through mass layoffs and communities sucked dry. Our national survival is imperiled as, once more, balance sheets and short-term transactions slam the door on jobs, workers, and even entrepreneurs. What can be done to ameliorate this issue? By closing the interest deduction loophole, companies will be prevented from deducting interest payments on debt (the debt the target company accumulated in the merger) to squeeze as much money as possible out of the company. This option encourages private-equity investors to take on large amounts of debt for acquisitions with no risk, making the company highly leveraged and financially at risk in the process. Additionally, private-equity firms often make the target company take on more debt to use the money to pay fast dividends, while this often risks the assets of the company and harms it finances. Outlawing debt-fueled dividends, which are inherently extractive and anti-productive, would be an important step in creating another hurdle for non-productivity-oriented private-equity acquisitions.

- Reconsideration of corporate governance and economic stakeholders.

A manner in which policymakers may reorient the mainstream understanding of corporate governance is by reversing the SEC measures that encourage shareholder primacy. It is the responsibility of American economic intellectuals, especially those who wish to champion this cause of economic restoration, to distill a more traditional view of corporate structuring that takes into account employees, communities, national interests, and second-order effects. What may be profitable for shareholders in the interim may not occasion sustainable policies, as is proven to be the case. An increase in share price does not translate into real growth–growth of wages, of industrial capacity, of defense production, and other important aspects of a national economy. American corporate law and SEC regulations should therefore no longer lend tacit approval to shareholder primacy.

- Bank regulations.

The federal government should no longer subsidize recklessness by guaranteeing banks in the event of failure. The government should hold banks accountable and let them deal with their own risk. A revival of the Glass-Steagall Act, especially Section 21, would prevent investment banks from receiving federally-insured deposits which would prevent the government from bailing out banks that lose the money of clients in their investments. With investment and commercial banks being separated, the economy will not be vulnerable to massive economic crashes because consumers and institutions alike would not lose everything as their assets would not be tied to large investment banks. For the survival of our economy, and for the potential for growth and reindustrialization, the imperial power of banks must be reduced.

Criticism of America’s fundamental economic ailments (not merely price increases and inflation) are disproportionately dominated by the left, who often attack capitalism in general from a left-wing economic point of view. Above all, now is not the time to, in our economic stupor, abandon capitalism. It is time to reinvigorate it. It is not time for a new New Deal, where the federal government will stifle the free market in its attempt to play the savior once again, but for a New Capitalism. A capitalism that is no less free and revering of the property right, yet one that takes into account broader stakeholders rather than just shareholders; a capitalism that serves workers and businessmen; a system of free enterprise that unleashes national strength.

References

Emerging Trends. (n.d.). [PDF file]. Stanford University. https://emergingtrends.stanford.edu/files/original/b47790c9061e2c5486e8914af8f2de4290d194d3.pdf

Reuters. (2025, April 11). There’s no easy escape from the U.S. bubble economy. https://www.reuters.com/breakingviews/theres-no-easy-escape-us-bubble-economy-2025-04-11/?utm

Krippner, G. (n.d.). [PDF file]. UNAM. https://www.depfe.unam.mx/actividades/10/financiarizacion/i-7-KrippnerGreta.pdf

Rappaport, A. (2006). The shareholder value myth: How putting shareholders first harms investors, corporations, and the public. Berrett-Koehler Publishers. https://www.amazon.com/Shareholder-Value-Myth-Shareholders-Corporations/dp/1605098132

FDIC. (1985). History of the eighties—Lessons for the future: An examination of the banking crises of the 1980s and early 1990s (Vol. 1). https://www.fdic.gov/bank/historical/history/3_85.pdf

FDIC. (n.d.). Deposit insurance. https://www.fdic.gov/resources/deposit-insurance

Wikipedia. (n.d.). Savings and loan crisis. https://en.wikipedia.org/wiki/Savings_and_loan_crisis

FDIC. (n.d.). Special banking review. https://www.fdic.gov/analysis/archived-research/banking-review/brspecial.pdf

[Author unknown]. (2003). [PDF file]. University of St Andrews. https://www.st-andrews.ac.uk/~wwwecon/repecfiles/4/2003.pdf

American Compass. (2021, March). Corporate erosion of capitalism. https://americancompass.org/wp-content/uploads/2021/03/AC-ResearchReport_Corporate-Erosion-of-Capitalism_Final_Updated.pdf

American Compass. (n.d.). Bringing back American investment. https://americancompass.org/rebuilding-american-capitalism/productive-markets/bringing-back-american-investment